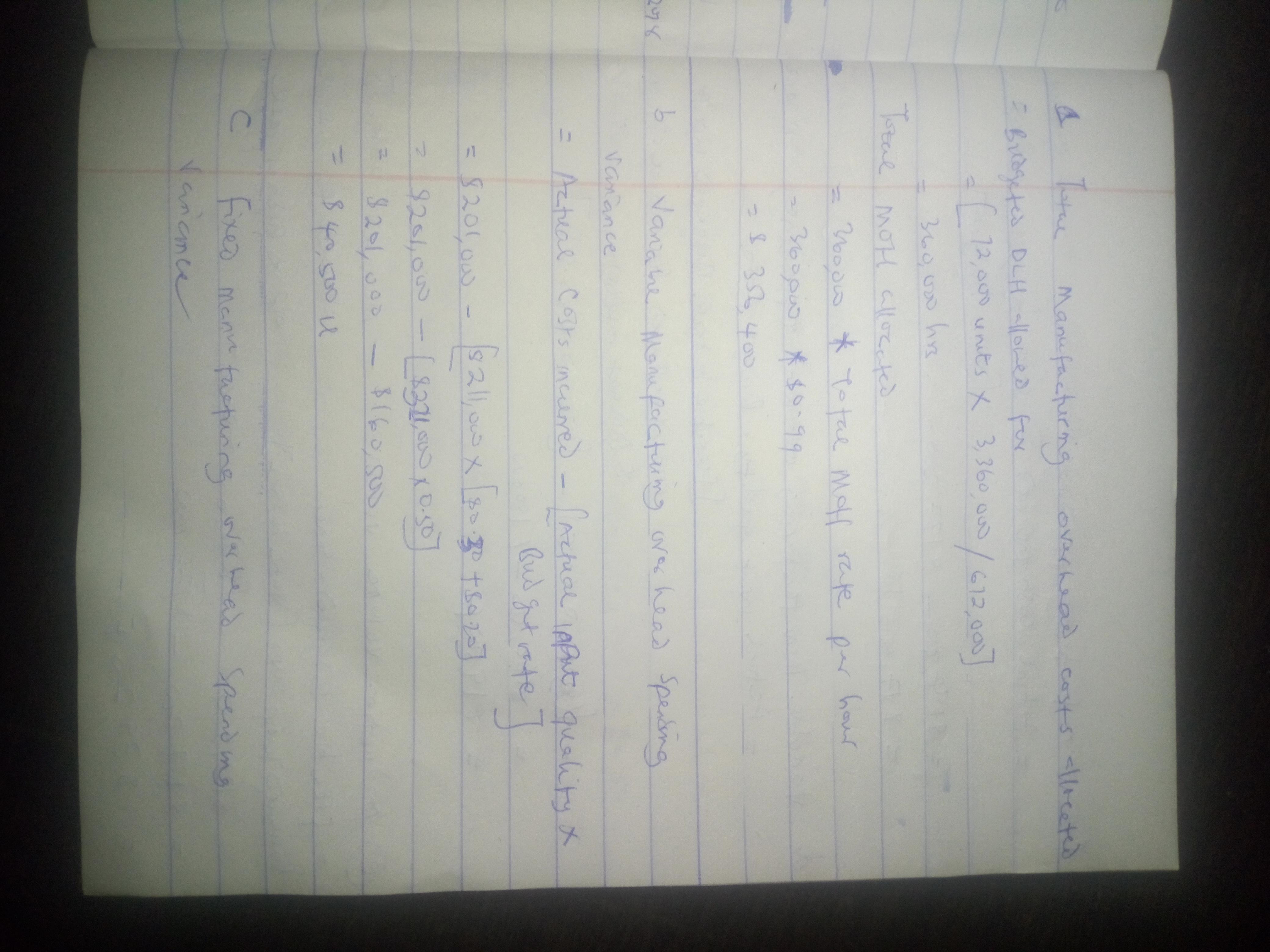

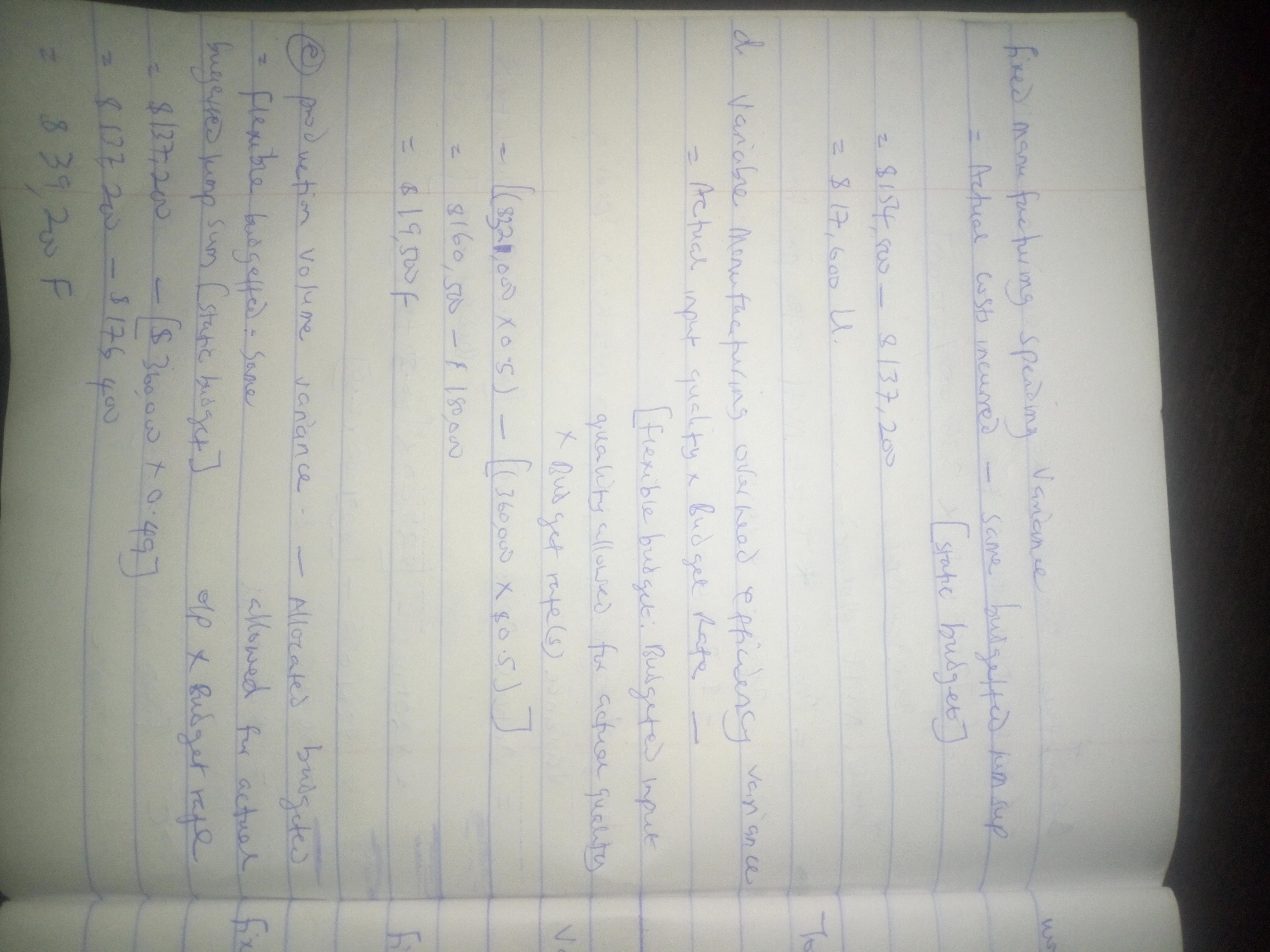

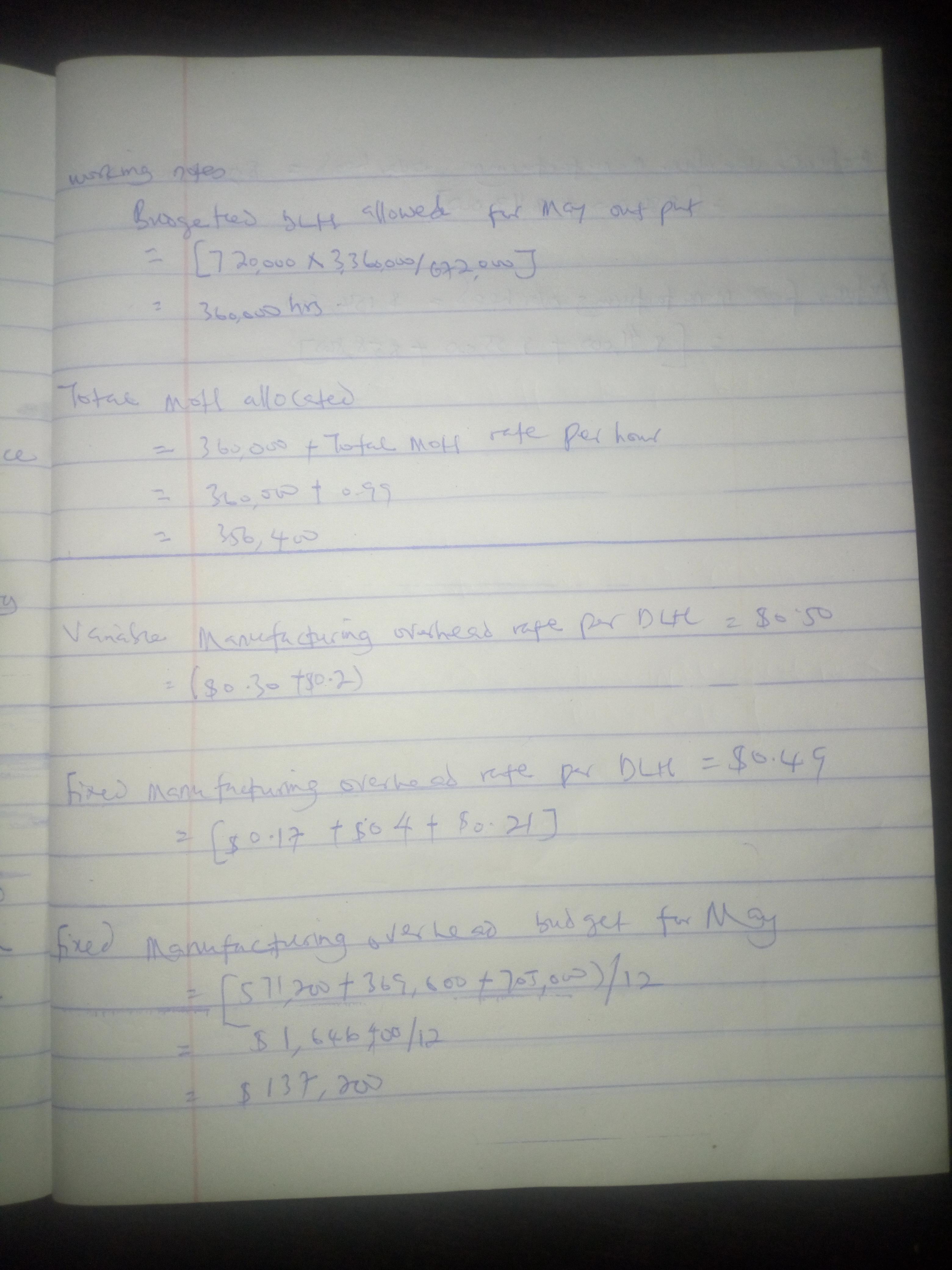

Wilson Products uses standard costing. It allocates manufacturing overhead (both variable and fixed) to products on the basis of standard direct manufacturing labor-hours (DLH). Wilson Products develops its manufacturing overhead rate from the current annual budget. The manufacturing overhead budget for 2014 is based on budgeted output of 672,000 units, requiring 3,360,000 DLH. The company is able to schedule production uniformly throughout the year.

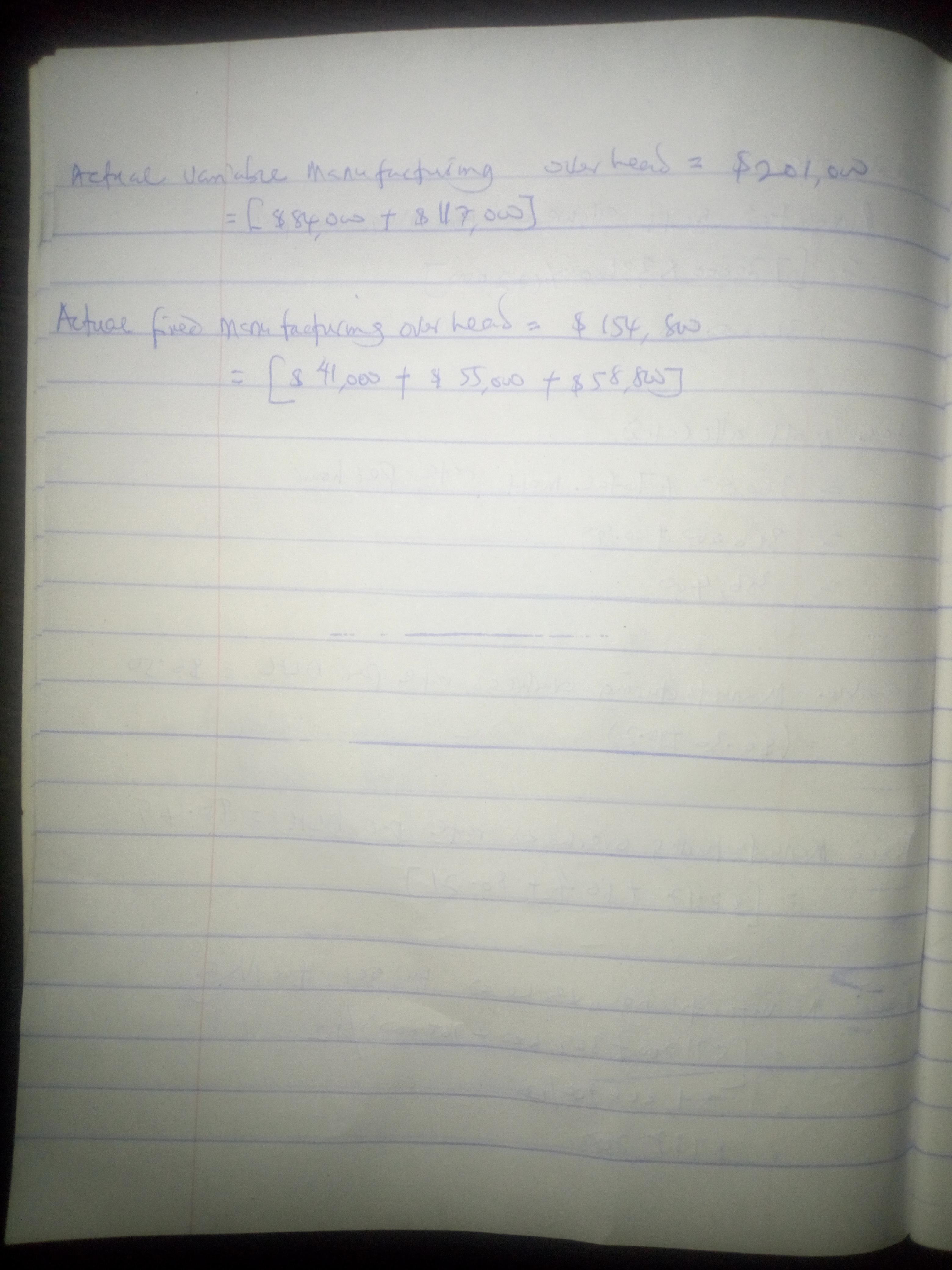

A total of 72,000 output units requiring 321,000 DLH was produced during May 2014. Manufacturing overhead (MOH) costs incurred for May amounted to $ 355,800. The actual costs, compared with the annual budget and 1/12 of the annual budget, are as follows:

Calculate the following amounts for Wilson Products for May 2014:

Total Amount Per Output Unit Per DLH Input Unit Monthly MOH Budget May 2017 Actual MOH Costs for May 2017

Variable MOH

Indirect manufacturing labor $1,008,000 $1.50 $0.30 $84,000 $84,000

Supplies 672,000 1.00 0.2 56,000 117,000

Fixed MOH

Supervision 571,200 0.85 0.17 47,600 41,000

Utilities 369,600 0.55 0.11 30,800 55,000

Depreciation 705,600 1.05 0.21 58,800 88,800

Total $33,26,400 $4.95 $0.99 $277,200 $355,800

Required:

a. Total manufacturing overhead costs allocated.

b. Variable manufacturing overhead spending variance.

c. Fixed manufacturing overhead spending variance.

d. Variable manufacturing overhead efficiency variance.

e. Production-volume variance Be sure to identify each variance as favorable (F) or unfavorable(U).

Answers

Answer:

Please see attached solution

Explanation:

a. Total manufacturing overhead costs allocated $356,400

b. Variable manufacturing overhead spending variance $40,500U

c. Fixed manufacturing overhead spending variance $17,600U

d. Variable manufacturing overhead efficiency variance $19,500F

e. Production volume variance $39,200F

Please find attached detailed solution to the above questions

Related Questions

Amanda is a twenty-four year old student. For two years Amanda has been going to gym and using weight equipment, stationary bicycles, and step machines to improve muscle tone. One spring afternoon Amanda was using a weight machines in the usual way (and the way she was showed how to use it), when the machine malfunctioned causing her serious injury. The company that made the machine, Musclematic, has known for the past year that this problem existed, but the company took no steps to warn people who owned or used these machines of the problem.

If Amanda files a lawsuit against Musclematic, the company might want to seriously consider:

a. How this litigation will affect its goodwill

b. Whether or not a settlement with Amanda is a viable option

c. Whether this suit will adversely affect other business relationships

d. The costs associated with litigating this claim

e. All of the other choices

Answers

Answer:

e. All of the other choices

Explanation:

Product liability is the responsibility that a company bears for injury caused by its products as a result of a defect.

In this instance Musclematic, has known for the past year that this problem existed, but the company took no steps to warn people who owned or used these machines of the problem.

So for any injury users have they will be liable.

If Amanda files a lawsuit against Musclematic they will have to consider:

- How this litigation will affect its goodwill

- Whether or not a settlement with Amanda is a viable option

- Whether this suit will adversely affect other business relationships

- The costs associated with litigating this claim

This is because they will most likely lose the case.

MotorCar, a major automobile company headquartered in Detroit, is concerned about being left behind in the race to produce autonomous vehicles. There remains much uncertainty regarding the future of autonomous vehicle technology. Some industry experts say fully self-driving cars could be brought to market within a couple of years. Others believe the technology could take decades to develop. And still others are skeptical that the technology will ever be safe enough to bring to the automobile mass market. Further, in addition to safety and technological hurdles, there are regulatory obstacles as well. However, MotorCar has decided that it needs to innovate.

The company is considering (1) increasing funding to its existing R&D department to expand to the development of AI (artificial intelligence) technology, needed for self-driving vehicles; (2) launching a fully owned subsidiary (a new company that it owns and controls) focused exclusively on AI; or (3) partnering with a major Silicon Valley tech company that has already made considerable progress on AI technology.

Required:

What do you see as some of the potential benefits and risks of these different organizational approaches?

Answers

Answer:

(1) increasing funding to its existing R&D department to expand to the development of AI (artificial intelligence) technology, needed for self-driving vehicles

This strategy would produce the benefit of puttinig the company on the edge of the development of AI in order to produce driverless vehicles.

The risk is that the investment could be too high for the initial benefit, since there is no certainty that driveless cars will be in the market in the short-term.

(2) launching a fully owned subsidiary (a new company that it owns and controls) focused exclusively on AI

This strategy would produce a similar benefit as the strategy above. However, it could also benefit from a little bit less administrative control because in this case, the AI development would be in charge of a subsidiary, not a division.

The risk is the same as above: initial investments may be too high for the initial benefits.

(3) partnering with a major Silicon Valley tech company that has already made considerable progress on AI technology.

This strategy produces the benefit of requiring less investment while still putting the company on the edge of AI research. However, the risk lies in loss of control over the thecnology, and possible future conflicts with the partner company.

Connors Corporation acquired manufacturing equipment for use in its assembly line. Below are four independent situations relating to the acquisition of the equipment. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

A. The equipment was purchased on account for $25,000. Credit terms were 2/10, n/30. Payment was made within the discount period and the company records the purchases of equipment net of discounts.

B. Connors gave the seller a noninterest-bearing note. The note required payment of $27,000 one year from date of purchase. The fair value of the equipment is not determinable. An interest rate of 10% properly reflects the time value of money in this situation.

C. Connors traded in old equipment that had a book value of $6,000 (original cost of $14,000 and accumulated depreciation of $8,000) and paid cash of $22,000. The old equipment had a fair value of $2,500 on the date of the exchange. The exchange has commercial substance.

D. Connors issued 1,000 shares of its nopar common stock in exchange for the equipment. The market value of the common stock was not determinable. The equipment could have been purchased for $24,000 in cash.

Required:

For each of the above situations, prepare the journal entry required to record the acquisition of the equipment.

Answers

Answer:

Entries and their narrations are posted below

Explanation:

We will record assets and expenses on the debit as they increase during the year and will record liabilities and capital on the credit side as they increase during the year or vice versa.

Journal Entries

Debit Credit

A. The equipment was purchased on account for $25,000.

Equipment $25,000

Accounts Payable $25,000

B. Connors gave the seller a noninterest-bearing note. The note required payment of (27,000 x 1/(1+10%)

Equipment $24,545

Discount on Notes Payable $2,455

Note Payable $27,000

C. Connors traded in old equipment that had a book value of $6,000

Equipment New $24,500

Accumulated Depreciation $8,000

Loss on Equipment $3,500

Cash $22,000

Equipment Old $14,000

D.Connors issued 1,000 shares of its nopar common stock in exchange for the equipment

Equipment $24,000

Common Stock $24,000

Tariff effects: An overview

Consider two hypothetical countries, Alagir and Ertil. Both countries produce iGadgets, and the price of iGadgets is lower in Alagir than in Ertil. If Alagir and Ertil open to trade, producers in would be more likely to lobby their government for an import tariff on iGadgets in order to protect themselves from foreign competition.

Which of the following statements about the effects of the tariff compared to free trade are correct?

A. In Alagir, workers in iGadget importing companies lose their jobs.

B. In Ertil, some workers at retail and shipping companies that import iGadgets lose their jobs.

C. In Ertil, consumers pay more for the domestic iGadgets.

D. In Ertil, workers in iGadget importing companies see more jobs available to them.

E. In Ertil, producers of iGadgets are willing to expand output.

Answers

Answer:

1. If Alagir and Ertil open to trade, producers in Ertil would be more likely to lobby their government for an import tariff on iGadgets in order to protect themselves from foreign competition.

Producers in Ertil would be at a disadvantage because people in Ertil would simply buy the lower priced iGadgets from Alagir so the producers in Ertil would lobby their Government for tariffs to protect them.

2.

B. In Ertil, some workers at retail and shipping companies that import iGadgets lose their jobs.If an import tariff is imposed, people will find the goods from Alagir more expensive and so will import less. The companies who did the shipping and retail of the goods from Alagir would have to let go of some people to save costs or because they would close down.

C. In Ertil, consumers pay more for the domestic iGadgets.With tariffs to protect them, the domestic producers in Ertil can charge higher prices.

E. In Ertil, producers of iGadgets are willing to expand output.With the tariff protecting them, the producers will be willing to expand output so that they can sell more iGadgets at the new higher price.

Consider the markets for three products below. Indicate which characteristics of a competitive market are met by these markets.

Market: gasoline

a. Large number of buyers unanswered

b. Standardized good unanswered

c. Full information unanswered

d. No transaction cost unanswered

e. Participants are price takers unanswered

Market: barbershop haircuts

a. Large number of buyers unanswered

b. Standardized good unanswered

c. Full information unanswered

d. No transaction cost unanswered

e. Participants are price takers unanswered

Market: bicycles

a. Large number of buyers unanswered

b. Standardized good unanswered

c. Full information unanswered

d. No transaction cost unanswered

e. Participants are price takers

Answers

Answer:

Market: gasoline (monopolistic competition with few sellers and many buyers)

a. Large number of buyers

b. Standardized good

c. Full information (not all participants know all the information, but most is available if they search for it)

d. No transaction cost

e. Participants are price takers

Market: barbershop haircuts (monopolistic competition with a lot of sellers and many buyers, but differentiated service)

a. Large number of buyers

d. No transaction cost

e. Participants are price takers

Market: bicycles (resembles a perfect competition market)

a. Large number of buyers

b. Standardized good

c. Full information (not all participants know all the information, but most is available if they search for it)

d. No transaction cost

e. Participants are price takers

Explanation:

No market provides full information to all participants. The closest you can get are some markets where commodities are traded and the price is set be certain exchange institutions. E.g. the Chicago Mercantile Exchange sets the price of agricultural commodities in the US, and most trading companies follow that price but variations still exist (even though they are minimum).

It is not possible for all the consumers of gasoline, haircuts or bicycles to know the exact price of all the goods the services since the price varies from one seller to another. Even if they are part of a retail chain, the price varies. Full information only exists in theoretical models, it doesn't exist in the real world.

Market: gasoline (monopolistic competition with few sellers and many buyers)

a. Large number of buyers

b. Standardized good

c. Full information (not all participants know all the information, but most is available if they search for it)

d. No transaction cost

e. Participants are price takers

Market: barbershop haircuts (monopolistic competition with a lot of sellers and many buyers, but differentiated service)

a. Large number of buyers

d. No transaction cost

e. Participants are price takers

Market: bicycles (resembles a perfect competition market)

a. Large number of buyers

b. Standardized good

c. Full information (not all participants know all the information, but most is available if they search for it)

d. No transaction cost

e. Participants are price takers

Explanation:

No market provides full information to all participants. The closest you can get are some markets where commodities are traded and the price is set be certain exchange institutions. E.g. the Chicago Mercantile Exchange sets the price of agricultural commodities in the US, and most trading companies follow that price but variations still exist (even though they are minimum).

It is not possible for all the consumers of gasoline, haircuts or bicycles to know the exact price of all the goods the services since the price varies from one seller to another. Even if they are part of a retail chain, the price varies. Full information only exists in theoretical models, it doesn't exist in the real world.

Bridgeport Inc. wishes to accumulate $1,092,000 by December 31, 2030, to retire bonds outstanding. The company deposits $168,000 on December 31, 2020, which will earn interest at 10% compounded quarterly, to help in the retirement of this debt. In addition, the company wants to know how much should be deposited at the end of each quarter for 10 years to ensure that $1,092,000 is available at the end of 2030. (The quarterly deposits will also earn at a rate of 10%, compounded quarterly.) (Round factor values to 5 decimal places, e.g. 1.25124 and final answer to 0 decimal places, e.g. 458,581.)

Answers

Answer: $9,479

Explanation:

The number of periods = 10 years * 4 quarters = 40 periods

Interest per quarter = 10%/4 = 2.5%

$168,000 has been deposited. The value of this cash after 10 years is;

= 168,000 ( 1 + 2.5%) ^ 40

= $451,090.72

Out of $1,090,000, the amount remaining is;

= $1,090,000 - 451,090.72

= $638,909.28

They need to deposit an annuity per quarter to get to $638,909.28.

Future Value of Annuity = Annuity * ([1 + I]^N - 1 )/I

638,909.28 = Annuity * [(1+0.025)^40 - 1] /0.025

638,909.28 = Annuity * 67.40255

Annuity = 638,909.28/67.40255

= $9,479

Fields Company has two manufacturing departments, forming and painting. The company uses the weighted-average method of process costing. At the beginning of the month, the forming department has 36,000 units in inventory, 70% complete as to materials and 30% complete as to conversion costs. The beginning inventory cost of $82,100 consisted of $58,000 of direct materials costs and $24,100 of conversion costs.

During the month, the forming department started 520,000 units. At the end of the month, the forming department had 40,000 units in ending inventory, 85% complete as to materials and 35% complete as to conversion. Units completed in the forming department are transferred to the painting department. Cost information for the forming department is as follows:

Beginning work in process inventory $82,100

Direct materials added during the month 1,942,930

Conversion added during the month 1,359,730

1A. Calculate the equivalent units of production for the forming department.

1B. Calculate the costs per equivalent unit of production for the forming department.

1C. Using the weighted-average method, assign costs to the forming department’s output—specifically, its units transferred to painting and its ending work in process inventory.

Answers

Answer:

Please see attached detailed solution

Explanation:

1a. Direct material 550,000

Conversion 530,000

1b. Direct materials $3.64 per EUP

Conversion $2.61 per EUP

1c. Costs assigned to the forming department's output

• Total cost of ending work in process $160,300

• Total costs assigned $3,384,760

Please see attached detailed solution to the above questions and answers.

Nanjones Company manufactures a line of products distributed nationally through wholesalers. Presented below are planned manufacturing data for the year and actual data for November of the current year. The company applies overhead based on planned machine hours using a predetermined annual rate.

Planning Data

Annual November

Fixed overhead $1,200,000 $100,000

Variable overhead $2,400,000 $220,000

Direct labor hours 48,000 4,000

Machine hours 240,000 22,000

Data for November

Direct labor hours (actual) 4,200

Direct labor hours (plan based on output) 4,000

Machine hours (actual) 21,600

Machine hours (plan based on output) 21,000

Fixed overhead $101,200

Variable overhead $214,000

Nanjones’ variable overhead spending variance for November was:

a. $6,000 favorable.

b. $2,000 favorable.

c. $14,000 unfavorable.

d. $6,000 unfavorable.

Answers

Answer:

Variable manufacturing overhead spending variance= $2,000 favorable

Explanation:

First, we need to calculate the predetermined overhead rate:

Predetermined manufacturing overhead rate= total estimated overhead costs for the period/ total amount of allocation base

Predetermined manufacturing overhead rate= 2,400,000 / 240,000

Predetermined manufacturing overhead rate= $10 per machine hour

To calculate the variable overhead spending variance, we need to use the following formula:

Variable manufacturing overhead spending variance= (standard rate - actual rate)* actual quantity

Variable manufacturing overhead spending variance= (15 - 214,000/21,600)*21,600

Variable manufacturing overhead spending variance= $2,000 favorable

The Nanjones' variable overhead spending variance for November is a. $6,000 favorable.

Data and Calculations:

Planning Data Actual Data Variances

Annual November November

Fixed overhead $1,200,000 $100,000 $101,200 $1,200 U

Variable overhead $2,400,000 $220,000 $214,000 $6,000 F

Direct labor hours 48,000 4,000 4,200 200 U

Machine hours 240,000 22,000 21,600 400 F

Thus, the Nanjones' variable overhead spending variance for November is the difference between planned expenses and actual expenses, which is $6,000 ($214,000 - $220,000) favorable.

Learn more about variable overhead spending variance here: https://brainly.com/question/4535958

Tasty Subs acquired a delivery truck on October 1, 2021, for $25,600. The company estimates a residual value of $1,600 and a six-year service life. Required: Calculate depreciation expense using the straight-line method for 2021 and 2022, assuming a December 31 year-end.

Answers

Answer:

Depreciation Expense 2021= $1,000

Depreciation Expense 2022= $4,000

Explanation:

Calculation for depreciation expense using the straight-line method for 2021 and 2022

Using this formula

Depreciation = ( Cost − Residual Value )/

Useful Life

Where,

Cost of Truck on October 1,2021= $25,600

Residual Value = $1,600

Useful life of truck = 6 years service life

Let plug in the formula

2021

Depreciation Expense = $25,600 - $1,600 / 6 years * 3/12

Depreciation Expense 2021= $1,000

Note October 1 to 31 December 2021 will give us 3 months

2022

Depreciation Expense=$25,600 - $1,600 / 6 years

Depreciation Expense 2022= $4,000

Therefore the Depreciation Expense for 2021 will be $1,000 while the Depreciation Expense for 2022 will be $4,000

A company has total equity of $2,160, net working capital of $240, long-term debt of $1,070, and current liabilities of $4,500. What is the company's net fixed assets?

Answers

Answer:

$2,990

Explanation:

A company's fixed asset consist of its plants and machineries, motor vehicles , buildings etc.

To get the company's net fixed asset, we would subtract the networking capital from total equity and add up long term debt.

Therefore,

Net fixed asset = $2,160 total equity - $240 working capital + $1,070 long term debt

= $2,990

Hence net fixed asset is $2,990

Which represents the best way to compose experience statements? a. Input 35+ accounts receivable using QuickBooks Prepared monthly billing statements and mailed them to customers Answered phones in busy office, referred customer billing questions to appropriate staff, and wrote e-mails to vendors b. Used QuickBooks to input accounts recievable Prepare monthly billing statements for customers Conducted general office duties such as phone inquiries, referring customers to proper staff, and I also wrote e-mails to vendors c. Responsible for inputting data for more than 35 accounts into QuickBooks Experienced with creating monthly billing statements to mail to customers As receptionist, I answered customer billing questions, wrote e-mails to vendors Skip

Answers

Full question read.

"You will graduate with a BA in accounting from the University of Texas in Austin in a few weeks. And saw an ad for a position in your hometown of San Antonio that matches your skill set. Your experience in your current job, in which you counted cash from various establishments around campus, and prepared daily deposit slips matches one of the full-time jobs requirements. Before that, you performed accounts receivable functions at a large construction company. Another requirement named in the job ad. You decide to apply for the position. Your task. Create a resume tailored to the position. "

This well-written objective customized for the job opening, includes strategic key words for applicant tracking systems and focuses on how the candidate can contribute to the organization. This bulleted list of employment history, most appropriately quantifies the candidates accomplishments.

Which represents the best way to compose experience statements?

Answer:

C. Responsible for inputting data for more than 35 accounts into QuickBooksExperienced with creating monthly billing statements to mail to customersAs receptionist, I answered customer billing questions, wrote e-mails to vendorsExplanation:

Remember, we are told that "strategic key words for applicant tracking systems..." would be used by the organization to determine the best candidates. It, therefore means that accurate spelling would make an experience statement compelling and detectable by the tracking system.

From the above statements, under these conditions, option c appears to be the best way to compose experience statements.

What are the 2 main sources of data

Answers

Answer:

internal and external source

Explanation:

Answer:

There are two sources of data. they are:

1. Internal Source.

2. External Source.

Explanation:

Internal Source. When data are collected from reports and records of the organision itself, it is known as the internal source.

External Source. When data are collected from outside the organition, it is known as the external source.

HELP ME PLSSS SOMEONE HELPP ILL GIVE BRAINLIEST

tom sold 3 cars ( a total value of $112,500) in the month of january. it is paid only by commission for its seller. he receives a commission of 7%. what is tom’s salary for the month of january?

Answers

Answer:

$7,875

Explanation:

Total car sales in January: $112,500

Commission at the rate of 7%,

Salary for January is :

7 percent of $112,500

=7/100 x $112,500

=0.07 x $112,500

=$7,875

Constructing and Assessing Income Statements Using Cost-to-Cost Method On March 15, 2014, Frankel Construction contracted to build a shopping center at a contract price of $125 million. The schedule of expected (which equals actual) cash collections and contract costs follow ($ millions):

Year Cash Collections Cost Incurred

2014 $30 $20

2015 50 45

2016 45 35

Total $125 $100

Required:

a. Calculate the amount of revenue, expense, and net income for each of the three years 2014 through 2016 using the cost-to-cost method.

b. What best summarizes our conclusion about the usefulness of the cost-to-cost method for this company?

Answers

Answer:

a. Net income in 2014 is $5.00 million; Net income in 2015 is $11.25 million; and Net income in 2016 is $8.75million.

b. The best summary is that under generally accepted accounting principles (GAAP), the cost-to-cost method is a method that is acceptable to be applied to contracts that span more than one accounting period.

Therefore, the cost-to-cost method is employed in calculating the revenue and net income for Frankel Construction for each of the years 2014, 2015 and 2016.

Explanation:

a. Calculate the amount of revenue, expense, and net income for each of the three years 2014 through 2016 using the cost-to-cost method.

Note: See the attached excel file for the calculations.

Cost-to-cost method can be described as a cost and revenue recognition approach in which all costs recorded to date on a project are divided by the total expected costs to be incurred on the project in order to obtain the overall percentage of completion of the project which is employed in estimating revenue and net income.

b. What best summarizes our conclusion about the usefulness of the cost-to-cost method for this company?

The best summary is that under generally accepted accounting principles (GAAP), the cost-to-cost method is a method that is acceptable to be applied to contracts that span more than one accounting period.

In this question, the cost-to-cost method is employed in calculating the revenue and net income for this company for each of the year 2014, 2015 and 2016.

The McMahon Construction Company builds bridges. In September and October 20XX, the company worked on a bridge covering the Kleinfeld River in Northern Montana. The McMahon Company has two departments, the Precast Department and the Construction Department. The Precast Department is responsible for building structural elements of bridges in temporary locations (plants) located near the construction sites. The Construction Department operates at the bridge site and they are responsible for assembling the precast structural elements. The estimated costs for Kleinfeld River Bridge for the Precast Department were $ 1,750,000 for direct materials, $ 240,000 for direct labor, and $300,000 for overhead. The estimated costs for the Construction Department regarding the Kleinfeld River Bridge were $ 400,000 for direct materials, $ 180,000 for direct labor, and $ 260,000 for overhead. Overhead is applied on the last day of the month. The Overhead application rate for the Precast Department is $ 30 per direct labor hour. The Overhead application for the Construction Department is 150 percent of direct labor cost.

Transactions for September

Sept 1- Purchased $ 1,170,000 of material on account for the Precast Department to start the building of structural elements. All of the material was issued to production, of the issuance amount, $ 720,000 is considered direct material.

Sept 4- Installed utilities at bridge site at a total cost of $30,000. The amount will be paid later in the month. (Transaction applies to Construction Department)

Sept 6-Paid rent for the temporary construction site housing the Precast Department, $ 7,200.

Sept 15- Completed the bridge support pillars by the Precast Department and transfer everything to the construction site.

Sept 19- Paid machine rental expense of $ 65,000 incurred by the Construction Department for clearing the bridge site and digging the foundations for bridge supports.

Sept 23- Purchased additional materials costing $1,510,000 on account.

Sept 30-The company paid the bills for the Precast Department: utilities, $ 7,200; direct labor, $50,000; insurance, $ 6,700, indirect labor, $ 8,200. Departmental depreciation was recorded, $21,500.

Sept 30-The company paid the bills for the Construction Department: utilities, $ 2,600; direct labor, $19,500; indirect labor, $6,100; and insurance, $ 2,500. Department depreciation was recorded on equipment, $ 9,450. Sept 30- Issued a check to pay for the material purchased on Sept 1 and Sept 23. Sept 30-Applied overhead to production in each department; 6,400 machine hours were worked in the Precast Department for September. Note: Direct Labor Costs for the Construction Department were $19,500.

Transactions for October

Oct 1- Transferred additional structural elements from the Precast Department to the construction site. The construction department incurred an expense of $ 7,000 to rent a crane.

Oct 4- Issued $1,010,000 of material to the Precast Department. Of this amount, $860,000 was considered direct.

Oct 7- Paid rent of cash of $ 7,500 in cash for the temporary site that is occupied by the Precast Department.

Oct 12-Issued $ 390,000 of material to the Construction Department. Of this amount, $ 220,000 was considered direct.

Oct 15-Transferred additional structural elements from the Precast Department to the construction site.

Oct 25-Transferred the final batch of structural elements from the Precast Department to the construction site.

Oct 29-Completed the bridge.

Oct 31-Paid the final bills for the month in the Precast Department: utilities, $ 14,000; direct labor, $120,000; insurance, $10,200; indirect labor, $18,300. Department depreciation was recorded, $21,500.

Oct 31-Paid the final bills for the month in the Construction Department: utilities, $ 5,300; direct labor, $144,500; indirect labor, $19,200; and insurance, $ 7,400. Depreciation was recorded on equipment was $9,450.

Oct 31-Applied overhead in each department. The precast department recorded 4,120 machine hours in October.

Oct 31-Billed the state of Montana for the completed bridge at the contract price of $3,850,000.

Oct 31-Please record the cost of the completed jobs to Finished Goods Inventory.

Required:

Journalize the entries for the preceding transactions. For purposes of this case study it is not necessary to transfer direct material and direct labor from one department to another.

Answers

Answer:

The McMahon Construction Company

Journal Entries:

Sept. 1:

Debit Precast Direct Materials Inventory $1,170,000

Credit Accounts Payable $1,170,000

To record the purchase of materials on account for Precast.

Debit Work in Process-Precast $720,000

Debit Manufacturing Overhead (Precast Dept.) $450,000

Credit Precast Direct Materials Inventory $1,170,000

Sept. 4:

Debit Manufacturing Overhead (Construction Dept.):

Utilities Expense $30,000

Credit Utilities Payable $30,000

To recorde utilities installed at bridge site.

Sept 6:

Debit Manufacturing Overhead (Precast Dept.):

Rent Expense $7,200

Credit Cash Account $7,200

To record the payment of rent for the temporary construction site.

Sept. 15:

No journal entries.

Sept 19:

Debit Manufacturing Overhead (Construction Dept.):

Machine Rental Expense $65,000

Credit Cash Account $65,000

To record the payment of machine rental expense

Sept. 23:

Debit Direct Materials Inventory $1,510,000

Credit Accounts Payable $1,510,000

To record the purchase of additional materials on account.

Sept. 30:

Debit:

Utilities Payable-Precast Dept $7,200

Direct labor -Precast Dept. $50,000

Debit Manufacturing Overhead (Precast Dept.):

Insurance Expense- Precast $6,700

Indirect labor $8,200

Credit Cash Account $72,100

Debit Manufacturing Overhead (Precast Dept.):

Depreciation Expense$21,500

Credit Accumulated Depreciation - Precast Dept $21,500

To record the depreciation expense for the month.

Sept. 30:

Debit Work in Process: Direct labor $19,500

Debit Manufacturing Overhead (Construction Dept.):

Utilities Expense t $2,600

Indirect labor $6,100

Insurance Expense $2,500

Credit Cash Account $30,700

Debit Manufacturing Overhead (Construction Dept.):

Depreciation Expense $9,450

Credit Accumulated Depreciation - Construction Dept $9,450

To record the depreciation expense for the month.

Debit Accounts Payable $2,680,000

Credit Cash Account $2,689,000

To record the payment on account by a check issued.

Debit Work in Process (Precast) $192,000

Credit Manufacturing Overhead (Precast) $192,000

To apply overhead to production in Precast Dept.

Debit Work in Process (Construction Dept.) $29,250

Credit Manufacturing Overhead (Construction Dept.) $9,250

To apply overhead to production in the construction department.

October:

Oct. 1:

Debit Manufacturing Overhead (Construction Dept.) $7,000

Credit Cash Account $7,000

To record the cost of rental a crane.

Oct. 4:

Debit Raw Materials Inventory (Precast) $860,000

Debit Manufacturing Overhead (Precast) $150,000

Credit Raw Materials Inventory.

Oct. 7:

Debit Manufacturing Overhead (Precast Dept.):

Rent Expense $7,500

Credit Cash Account $7,500

To record the payment of rent for cash.

Oct. 12:

Debit Work in Process (Construction Dept.) $220,000

Debit Manufacturing overhead-170,000

Credit Raw Materials $390,000

To record the issue of materials to the construction dept.

Oct. 15:

No Journal Entries required

Oct. 25:

No Journal Entries required

Oct. 29:

No. Journal Required

Oct. 31:

Debit:

Work in Process (Direct labor) $120,000

Manufacturing Overhead (Precast):

Utilities $14,000

Insurance $10,200

Indirect labor $18,300

Credit Cash Account $162,500

Oct. 31:

Debit Manufacturing Overhead (Precast Dept.):

Depreciation Expense$21,500

Credit Accumulated Depreciation - Precast Dept $21,500

To record the depreciation expense for the month.

Oct 31:

Debit Work in Process: Direct labor $144,500

Debit Manufacturing (Construction Dept.):

Utilities Expense t $5,300

Indirect labor $19,200

Insurance Expense $7,400

Credit Cash Account $176,400

To record the payment of cash for the expense

Debit Manufacturing Overhead (Construction Dept.):

Depreciation Expense $9,450

Credit Accumulated Depreciation - Construction Dept $9,450

To record the depreciation expense for the month.

Debit Work in Process (Precast) $123,600

Credit Manufacturing Overhead (Precast) $123,600

To apply overhead to production in Precast Dept.

Debit Work in Process (Construction Dept.) $216,750

Credit Manufacturing Overhead (Construction Dept.) $216,750

To apply overhead to production in the construction department.

Debit Accounts Receivable (State of Montana) $3,850,000

Credit Service Revenue $3,850,000

To record the billing of the state for the completed bridge.

Debit Finished Goods Inventory $1,835,600

Credit Work in Process $1,835,600

To record the cost of the completed jobs.

Explanation:

a) Data:

Estimated costs for Kleinfeld River Bridge

Precast Construction

Department Department

Direct materials $ 1,750,000 $ 400,000

Direct labor 240,000 180,000

Overhead 300,000 260,000

Overhead application $30 per DMH 150% DL

Machine hours worked 6,400 MH $19,500

Work in Process:

Materials $720,000

Direct labor (precast) 50,000

Direct labor (construction) 19,500

Overhead applied 192,000

Overhead applied 29,250

Materials 220,000

Direct labor 120,000

Direct labor 144,500

Overhead applied 123,600

Overhead applied 216,750

Total cost $1,835,600

Selected Information from Balance Sheets (As of Year End for Years 0 and 1)

Year 0 Year 1

Cash 1,000 2,000

Accounts Receivables 1,000 5,000

Inventory 5,000 4,000

Property, Plant and Equipment (net) 12,000 11,000

Accounts Payable 5,000 4,000

Unearned Revenue 2,000 1,000

Bonds Payable 5,000 6,000

Common Stock 3,000 4,000

Retained Earnings 5,000 7,000

Income Statement (Year 1)

Sales 20,000

Costs of Goods Sold (8,000)

Wage Expense (4,000)

Depreciation Expense (2,000)

Loss from PP&E Sale (1,000)

Net Income Before Tax 5,000

Tax Expense (2.000)

Net Income 3.000

In the space provided, prepare the Operating section of the statement of cash flow for Year 1, using the indirect approach.

Answers

Answer:

The Operating Activities section of the Statement of Cash Flow for Year 1:

Net Income $3,000

Add non-cash expenses:

Depreciation Expense 2,000

Loss from PP&E Sale 1,000

Operating cash flow 6,000

Changes working capital -5,000

Net cash flow from operating activities 1,000

Explanation:

Changes in working capital items:

Year 0 Year 1 Changes

Accounts Receivables 1,000 5,000 -4,000

Inventory 5,000 4,000 1,000

Accounts Payable 5,000 4,000 -1,000

Unearned Revenue 2,000 1,000 -1000

Net changes in working capital -5,000

For example, in 2012, each of the 80 billion pieces of advertising brought 21 cents in revenue, compared to 42 cents for first-class mail. Which word could best replace revenue in this sentence

Answers

Answer:

Returns

Explanation:

Returns on an investor is the amount of profit or gain an outlay of cash is able to bring at the end of a period.

Rate of returns on invested funds is used as a yardstick by potential investors in deciding which enterprise to fund.

In the given instance where each of the 80 billion pieces of advertising brought 21 cents in revenue, a better replacement for the word revenue is return.

So returns of funds invested on each piece of advertising is 21 cents.

Answer: income

Explanation:

synonym for revenue

Ballou Corporation declared a cash dividend on December 13, 2018, payable on January 10, 2019. By mistake, the company failed to make a journal entry in December 2018. The effect of this error on the financial statements as of December 31, 2018 were:_____.

a. retained earnings was overstated and liabilities were understated.

b. retained earnings was overstated and cash were understated.

c. retained earnings and liabilities were both understated.

d. retained earnings and liabilities were both overstated.

Answers

Answer: a. retained earnings was overstated and liabilities were understated.

Explanation:

Dividends are paid from the Retained Earnings so when a company announces a dividend, that dividend is to be deducted from the Retained earnings. As this was not done, the Retained earnings at year end are overstated.

As the dividends are not paid immediately, they become liabilities. With the relevant entries not made, the dividends were not recorded as liabilities which makes liabilities understated.

The environmental protection agency of a county would like to preserve a piece of land as a wilderness area. The current owner has offered to lease the land to the county for 20 years in return for a lump-sum payment of $1.1 million, which would be paid at the beginning of the 20-year period. The agency has estimated that the land would generate $110,000 per year in benefits to hunters, bird watchers, and hikers. Assume that the lease price represents the social opportunity cost of the land and that the appropriate real discount rate is 4 percent.

a. Assuming that the yearly benefits, which are measured in real dollars, accrue at the end of each of the 20 years, calculate the net benefits of leasing the land. Should the environmental protection agency pay for this piece of land?

b. Some analysts in the agency argue that the annual real benefits are likely to grow at a rate of 2 percent per year due to increasing population and county income. Recalculate the net benefits assuming that they are correct. Should the environmental protection agency pay for this piece of land?

Answers

Answer: Check explanation

Explanation:

a. For this scenario, it should be noted that the net benefits for the land lease will be equal to the present value of the benefits that are generated. This will be the annual benefit multiplied by the present value of annuity factor. This will be:

= $110,000 x 13.59

= $1,494,900

From the calculation, we can see that the lease price is less than the present value calculated, this implies that the transaction will incur a profit and should be undertaken.

b. For the growing annuity here, the calculation will be:

= [$110,000/(4% - 2%)] x [1 - [(1 + 2%)/(1 + 4%)]²⁰]

= [$110,000/2%] × [1 - (1 + 0.02)/(1 + 0.04)²⁰]

= $5,500,000 x 0.321833005

= $1,770,081.53

The environmental agency should pay for the piece of land as the present value calculated is higher.

Note that the present value of the annuity factor for 20 years at 4% = 13.59

10. ________________ is the extent to which employees have positive or negative feelings about various aspects of their work.

Answers

Answer:

A. Job satisfaction

Explanation:

Job satisfaction can be influenced by a number of significant factors. There may be motivation or lack of motivation according to the working conditions, such as job perception, management, organizational culture, reward system, etc.

There needs to be active management to analyze what are the main factors that affect job satisfaction in an organization, so that there is greater motivation, productivity, positive business climate, ethical behaviors, etc.

Your client, Bob, is the CEO of a corporation that has 12 stockholders who are also the only employees of the business. The corporation operates a boat dealership in Sherman, Texas. The corporation has accumulated earnings and profits of $3,000,000, not including the current year’s taxable income, which is expected to be $800,000. No dividends have been paid to stockholders. Bob has been very pleased with the corporation’s performance and he wants to reward the stockholders.

1. Why should Bob declare a cash dividend over giving stockholders a bonus?2. Why should Bob not consider paying a larger year-end bonus to his employee/stockholders’

Answers

Answer:

1. Why should Bob declare a cash dividend over giving stockholders a bonus?

Bob should not declare a cash dividend, instead he should give the employees/stockholders a bonus. A corporation distributes dividends with their after tax income, while bonuses actually decrease net income and lowers taxes. it is always better to pay less taxes.

2. Why should Bob not consider paying a larger year-end bonus to his employee/stockholders’.

In this case, if you have to choose between declaring a dividend or paying a bonus, Bob should definitely pay a bonus. But the bonus should not be larger than the corporation's expected income. It is not a good idea to incur in an operating loss due to huge bonuses.

Farr Corp. purchased a new delivery van on January 1, 2020 and chose to use the double declining balance depreciation method. The van cost $48,000 with an estimated life of five years and a $12,000 salvage value. After the year end adjustment, how much accumulated depreciation would be recorded on the van at December 31, 2021

Answers

Answer:

$30,720

Explanation:

First, we will calculate the depreciation for 2020.

Depreciation for 2020 = ($48,000 cost - 0) × 40%

= $19,200

Depreciation for 2021 = ($48,000 cost - $19,200 depreciation 2020) × 40%

= $11,520

Accumulated depreciation at the end of 2021

= $11,520 + $19,200

= $30,720

The value of $30,720 will be recorded as accumulated depreciation on the value of the van at December 31, 2021.

• Note, the asset's annual depreciation will be 20% of the depreciation cost since its useful life is 5. It will however be 40% since we are using the double declining balance method.

Ayayai Inc. wishes to accumulate $1,066,000 by December 31, 2030, to retire bonds outstanding. The company deposits $164,000 on December 31, 2020, which will earn interest at 8% compounded quarterly, to help in the retirement of this debt. In addition, the company wants to know how much should be deposited at the end of each quarter for 10 years to ensure that $1,066,000 is available at the end of 2030.

Answers

Answer:

Quarterly deposit= $11,653.28

Explanation:

Future Value= $1,066,000

Number of periods= 10*4= 40 quarters

Interest rate= 0.08/4= 0.02

First, we need to calculate the future value of the initial investment. Then, determine the difference required to reach the objective.

FV= PV*(1+i)^n

FV= 164,000*(1.02^40)

FV= $362,118.50

Difference= 1,066,000 - 362,118.5= $703,881.5

To calculate the quarterly deposit, we need to use the following formula:

FV= {A*[(1+i)^n-1]}/i

A= quarterly deposit

Isolating A:

A= (FV*i)/{[(1+i)^n]-1}

A= (703,881.5*0.02) / [(1.02^40) - 1]

A= $11,653.28

Carving Creations jointly produces wood chips and sawdust used in agriculture. The wood chips and sawdust are actually by-products of the company’s core operations, but Carving Creations accounts for them just like normally produced goods because of their large volumes. One jointly produced batch yields 3,000 cubic yards of wood chips and 10,000 cubic yards of sawdust, and the estimated cost per batch is $21,400. However, the joint production of each good is not equally weighted. Management at Carving Creations estimates that for the time it takes to produce 10 cubic yards of wood chips in the joint production process, only 2 cubic yards of sawdust are produced.

Given this information, allocate the joint costs of production to each product using the weighted average method.

Joint Product Allocation

Sawdust _____$

Wood chips _____

Totals _____ $

Answers

Answer:

Carving Creations

Joint Product Allocation

Sawdust _____$ 12,840 ($0.428 * 30,000)

Wood chips _____ $8,560 ($0.428 * 20,000)

Totals _____ $21,400

Explanation:

a) Data and Calculations:

Wood chips = 3,000 cubic yards

Sawdust = 10,000 cubic yards

Estimated batch cost = $21,400

Weight assigned to wood chips production = 10

Weight assigned to sawdust production = 2

Weighted Allocation of the joint costs:

Wood chips = 3,000 * 10 = 30,000

Sawdust = 10,000 * 2 = 20,000

Total weighted units = 50,000

Allocation rate based on weights = $21,400/50,000

= $0.428

Joint Product Allocation

Sawdust _____$ 12,840 ($0.428 * 30,000)

Wood chips _____ $8,560 ($0.428 * 20,000)

Totals _____ $21,400

Tara Foods of Georgia produces a wide range of peanut butters and food extracts, but does not sell any of its output under its own brand name.Tara evidently produces __________ .

Answers

Answer:

Middlemen's brands

Explanation:

A middlemen's brand can be defined as a type of business in which a manufacturing company that is into the production of goods sells its products to either a wholesaler, retailer without adding their brand name. Thus, this middlemen then sell the product with their own brand name.

In this scenario, Tara Foods of Georgia produces a wide range of peanut butters and food extracts, but does not sell any of its output under its own brand name.Tara evidently produces middlemen's brands.

Carol wants to invest money in a 6% Certificate of Deposit (CD) that compounds semiannually. Carol would like the account to have a balance of $50,000 five years from now. How much must Carol deposit to accomplish her goal

Answers

Answer:

the present value is $37,230.10

Explanation:

The computation of the present value is shown below:

As we know that

Future value = Present value × (1 + rate of interest)^time period

$50,000 = Present value × (1 + 0.06 ÷ 2)^5 × 2

$50,000 = Present value × (1.03)^10

$50,000 = Present value × 1.343

So, the present value is $37,230.10

hence, the present value is $37,230.10

We simply applied the above formula

Global strategic planning is a primary function of a company's managers, and the process of strategic planning provides a formal structure for undertaking this process. Companies are confronting a set of environmental forces that are increasingly complex, global, and subject to rapid change. In response, many international firms have found it necessary to institute formal global strategic planning to provide a means for top management to identify opportunities and threats from all over the world.

Required:

Formulate strategies to handle them, and stipulate how to finance and manage the implementation of these strategies?

Answers

Answer and Explanation:

The steps in global strategic planning include

Review or develop Vision & Mission: business aims to understand what its vision and mission is, reviewing one already there or developing a new one based on the current business environment and changes

Business and operation analysis. Here the business aims to understand it's environment in terms of it strengths and weaknesses internally and externally

Develop Strategic Options: business looks to find all strategic options available and weighs options to select best strategy on the basis of its business and operation analysis to understand strategy to tackle the current business situation

Establish Strategic Objectives: strategy objectives are developed to tackle new business environment

Strategy Execution Plan: the execution plan involves an effective plan that can duly implemented

Establish Resource Allocation: resources are allocated to execute the global strategic plan

Execution Review: execution is reviewed and quantified to see if the plan is being met

All of the current year's entries for Zimmerman Company have been made, except the following adjusting entries. The company's annual accounting year ends on December 31

On September 1 of the current year, Zimmerman collected six months' rent of $8,520 on storage space. At that date, Zimmerman debited Cash and credited Unearned Rent Revenue for $8,520.

On October 1 of the current year, the company borrowed $13,200 from a local bank and signed a one-year, 12 percent note for that amount. The principal and interest are payable on the maturity date.

Depreciation of $3,000 must be recognized on a service truck purchased in July of the current year at a cost of $24,000.

Cash of $3,600 was collected on November of the current year, for services to be rendered evenly over the next year beginning on November 1 of the current year. Unearned Service Revenue was credited when the cash was received.

On November 1 of the current year, Zimmerman paid a one-year premium for property insurance, $9,960, for coverage starting on that date. Cash was credited and Prepaid Insurance was debited for this amount.

The company earned service revenue of $4,200 on a special job that was completed December 29 of the current year. Collection will be made during January of the next year. No entry has been recorded.

At December 31 of the current year, wages earned by employees totaled $13,700. The employees will be paid on the next payroll date in January of the next year.

On December 31 of the current year, the company estimated it owed $490 for this year's property taxes on land. The tax will be paid when the bill is received in January of next year.

2. Using the following headings, indicate the effect of each adjusting entry and the amount of the effect. Use + for increase, − for decrease. (Reminder: Assets = Liabilities + Stockholders’ Equity; Revenues – Expenses = Net Income; and Net Income accounts are closed to Retained Earnings, a part of Stockholders’ Equity.)

Answers

Answer:

1) adjusting entries

a. On September 1 of the current year, Zimmerman collected six months' rent of $8,520 on storage space. At that date, Zimmerman debited Cash and credited Unearned Rent Revenue for $8,520.

Dr Unearned rental revenue 5,500

Cr Rental revenue 5,500

b. On October 1 of the current year, the company borrowed $13,200 from a local bank and signed a one-year, 12 percent note for that amount. The principal and interest are payable on the maturity date.

Dr Interest expense 396

Cr Interest payable 396

c. Depreciation of $3,000 must be recognized on a service truck purchased in July of the current year at a cost of $24,000.

Dr Depreciation expense 3,000

Cr Accumulated depreciation 3,000

d. Cash of $3,600 was collected on November of the current year, for services to be rendered evenly over the next year beginning on November 1 of the current year. Unearned Service Revenue was credited when the cash was received.

Dr Unearned service revenue 600

Cr Service revenue 600

e. On November 1 of the current year, Zimmerman paid a one-year premium for property insurance, $9,960, for coverage starting on that date. Cash was credited and Prepaid Insurance was debited for this amount.

Dr Insurance expense 1,660

Cr Prepaid insurance 1,660

f. The company earned service revenue of $4,200 on a special job that was completed December 29 of the current year. Collection will be made during January of the next year. No entry has been recorded.

Dr Accounts receivable 4,200

Cr Service revenue 4,200

g. At December 31 of the current year, wages earned by employees totaled $13,700. The employees will be paid on the next payroll date in January of the next year.

Dr Wages expense 13,700

Cr Wages payable 13,700

h. On December 31 of the current year, the company estimated it owed $490 for this year's property taxes on land. The tax will be paid when the bill is received in January of next year.

Dr Property taxes expense 490

Cr Property taxes payable 490

2) Assets = Liabilities + Stockholders’ Revenues - Expenses = Net

Equity Income

a. na - + + na +

b. na - - na - -

c. - na - na - -

d. na - + + na +

e. - na - na - -

f. + na + + na +

g. na + - na - -

h. na + - na - -

Jeremy is married to Amy, who abandoned him in 2019. He has not seen or communicated with her since April of that year. He maintains a household in which their son, Evan, lives. Evan is age 25 and earns over $6,000 each year. For tax year 2020, Jeremy's filing status is: a.Head of household. b.Surviving spouse. c.Married, filing jointly. d.Married, filing separately.

Answers

Answer: d. Married, filing separately.

Explanation:

From the question, we are informed that Jeremy is married to Amy, who abandoned him in 2019 and that he has not seen or communicated with her since April of that year.

We are further told that he maintains a household in which their son, Evan, lives and that Evan is age 25 and earns over $6,000 each year.

For tax year 2020, Jeremy's filing status is married, filling separately. This is because we are told that Jeremy hasn't has not seen or communicated with her since April. Since they're not divorced, it means they're still married but filing separately.

On December 31, 2021, the end of the fiscal year, California Microtech Corporation completed the sale of its semiconductor business for $15 million. The semiconductor business segment qualifies as a component of the entity according to GAAP. The book value of the assets of the segment was $13 million. The loss from operations of the segment during 2021 was $4.8 million. Pretax income from continuing operations for the year totaled $7.8 million. The income tax rate is 25%.

Prepare the lower portion of the 2021 income statement beginning with income from continuing operations before income taxes. Ignore EPS disclosures. (Amounts to be deducted and negative amounts should be indicated with a minus sign. Enter your answers in whole dollars and not in millions.)

Answers

Answer and Explanation:

The preparation of the lower portion is presented below:

Income from the continuing operation

before income tax $7,800,000

Less: Income tax expenses ($7,800,000 × 25%) (1,950,000)

Income from continuing operation(A) 5,850,000

Discontinued operation:

Loss from operation discontinued components

($15 - $13 - $4.8) ($2,800,000)

Income tax benefits ($2,800,000 × 25%) $700,000

Loss on discontinued operation(B) ($21,000,000)

Net loss (A - B) -$15,150,000